💡 Double entry accounting is a record keeping system under which every transaction is recorded in at least two accounts.

There is no limit on the number of accounts that may be used in a transaction, but the minimum is two accounts. There are two columns in each account, with debit entries on the left and credit entries on the right. In double entry accounting, the total of all debit entries must match the total of all credit entries. When this happens, the transaction is said to be "in balance." If the totals do not agree, the transaction is said to be "out of balance," and cannot be posted .Posted transactions are used to create financial statements.

Double entry accounting definitions

The definitions of a debit and credit are:

- A debit is that portion of an accounting entry that either increases an asset or expense account, or decreases a liability or equity account. It is positioned to the left in an accounting entry.

- A credit is that portion of an accounting entry that either increases a liability or equity account, or decreases an asset or expense account. It is positioned to the right in an accounting entry.

An account is a separate, detailed record associated with a specific asset, liability, equity, revenue, expense, gain, or loss.

Examples of accounts are:

- Cash (asset account: normally a debit balance)

- Accounts receivable (asset account: normally a debit balance)

- Inventory (asset account: normally a debit balance)

- Fixed assets (asset account: normally a debit balance)

- Accounts payable (liability account: normally a credit balance)

- Accrued liabilities (liability account: normally a credit balance)

- Notes payable (liability account: normally a credit balance)

- Common stock (equity account: normally a credit balance)

- Retained earnings (equity account: normally a credit balance)

- Revenue - products (revenue account: normally a credit balance)

- Revenue - services (revenue account: normally a credit balance)

- Revenue - products (revenue account: normally a credit balance)

- Cost of goods sold (expense account: normally a debit balance)

- Wage expense (expense account: normally a debit balance)

- Utilities (expense account: normally a debit balance)

- Travel and entertainment (expense account: normally a debit balance)

- Gain on sale of asset (gain account: normally a credit balance)

- Loss on sale of asset (loss account: normally a debit balance)

Double entry accounting examples

The definitions of a debit and credit are:

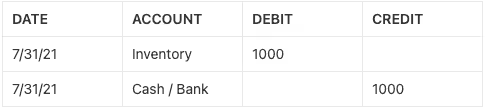

Buy merchandise

You buy $1,000 of goods with the intention of later selling them to a third party. The entry is a debit to the inventory (asset) account and a credit to the cash (asset) account. In this case, you are swapping one asset (cash) for another asset (inventory).

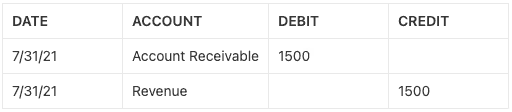

Sell goods

You sell the goods to a buyer for $1,500. There are two entries in this situation. One is a debit to the accounts receivable account for $1,500 and a credit to the revenue account for $1,500. This means that you are recording revenue while also recording an asset (accounts receivable) which represents the amount that the customer now owes you.

The second entry is a $1,000 debit to the cost of goods sold (expense) account and a credit in the same amount to the inventory (asset) account.

This records the elimination of the inventory asset as we charge it to expense. When netted together, the cost of goods sold of $1,000 and the revenue of $1,500 result in a profit of $500.

Pay employees

You pay employees $5,000. This is a debit to the wage (expense) account and a credit to the cash (asset) account. This means that you are consuming the cash asset by paying employees.

Buy a fixed asset

You pay a supplier $4,000 for a machine. The entry is a debit of $4,000 to the fixed assets (asset) account and a credit of $4,000 to the cash (asset) account. In this case, you are swapping one asset (cash) for another asset (inventory).

Incur debt

You borrow $10,000 from the bank. The entry is a debit of $10,000 to the cash (asset) account and a credit of $10,000 to the notes payable (liability) account. Thus, you are incurring a liability in order to obtain cash.

Sell shares

You sell $8,000 of shares to investors. The entry is a debit of $8,000 to the cash (asset) account and a credit of $8,000 to the common stock (equity) account.

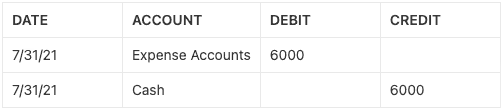

Pay a credit card statement

You pay a credit card statement in the amount of $6,000, and all of the purchases are for expenses. The entry is a total of $6,000 debited to several expense accounts and $6,000 credited to the cash (asset) account. Thus, you are consuming an asset by paying for various expenses.

Thus, the key point with double entry accounting is that a single transaction always triggers a recordation in at least two accounts, as assets and liabilities gradually flow through a business and are converted into revenues, expenses, gains, and losses.

Key terms used when recording financial transactions

A

journal is a place of record in which

business transactions are recorded in chronological order. A firm may use several specialised journals, such as a purchase journal or sales journal to separately record transactions. A general journal can be used to record more general, lower-volume transactions.Journals are the best source of information when researching the nature of business transactions, since they identify source documentsEntries made into a journal employ double-entry accounting, where balancing debit and credits are used. The entries also state the date, accounts impacted, and amounts, as well as an identifier for the source document.

Article Information

✍🏻 Written by: Eleven Support Team

🔎 Reviewed by: Noe Saglio

🗓️ Last Updated: November 12, 2025