Accounts (GL)

A general ledger account is an account or record used to sort, store and summarise a company's transactions. These accounts are arranged in the general ledger (and in the chart of accounts) with the balance sheet accounts appearing first followed by the income statement accounts.

Accounts Receivable & Accounts Payable

Accounts receivable is money that people owe you for goods and services. It’s considered an asset on your balance sheet. For example, if a customer fulfils their invoice your company’s accounts receivable amount is reduced because less money is now owed.Accounts payable is money that you owe other people and is considered a liability on your balance sheet. For example, let’s say your company pays $5,000 in rent each month. Here’s how that would be recorded in your financial records before that amount is paid out.

Once that value is paid, here’s how that would be recorded in your company’s financial records:

Accrual Accounting

The accrual method recognises revenue and expenses on the day the transaction takes place, regardless of whether or not it’s been received or paid. This method is more commonly used as it more accurately depicts the performance of a business over time.

Accruals

Accruals are revenues earned or expenses incurred that impact a company's net income on the income statement, although cash related to the transaction has not yet changed hands. Accruals also affect the balance sheet, as they involve non-cash assets and liabilities.

For example, if a company has performed a service for a customer, but has not yet received payment, the revenue from that service would be recorded as an accrual in the company's financial statements. This ensures that the company's financial statements accurately reflect its true financial position, even if it has not yet received payment for all of the services it has provided.

Accrual accounts include, among many others, accounts payable, accounts receivable, accrued tax liabilities, and accrued interest earned or payable.

Aging

Both A/P and A/R accounts include aging, which is simply a way to manage monies coming in or monies going out. A/P aging displays a list of all bills currently owed vendors and suppliers, tracking due dates and advising you when a payment is due, or when it is late.A/R provides the same information for outstanding customer payments, again advising you when a customer payment is late. Once you have multiple customers or vendors, aging reports can become invaluable to your business.

Assets

Assets are everything that your company owns — tangible and intangible. Your assets could include cash, tools, property, copyrights, patents, and trademarks.

Assets Book Value

For a tangible asset, the book value is calculated by subtracting depreciation from its original cost. If there have been any additional improvements to the asset, the cost of those may be added to its original cost.For example, The Cake Company bought a box-making machine for $11,000. After five years, the machine has depreciated at a rate of $1000 per year (using straight line depreciation). Its book value is now $6000.

Balance Sheet Report

The balance sheet is a report that summarises all of an entity's assets, liabilities, and equity for a selected period. It is typically used by lenders, investors, and creditors to estimate the liquidity of a business. The balance sheet is one of the documents included in an entity's financial statements.

Typical line items included in the balance sheet (by general category) are:

- Assets: Cash, marketable securities, prepaid expenses, accounts receivable, inventory, and fixed assets

- Liabilities: Accounts payable, accrued liabilities, taxes payable, short-term debt, and long-term debt

- Shareholders' equity: Stock, retained earnings, and treasury stock

The exact set of line items included in a balance sheet will depend upon the types of business transactions with which an organisation is involved. Usually, the line items used for the balance sheets of companies located in the same industry will be similar, since they all deal with the same types of transactions. The line items are presented in their order of liquidity, which means that the assets most easily convertible into cash are listed first, and those liabilities due for settlement soonest are listed first.

The total amount of assets listed on the balance sheet should always equal the total of all liabilities and equity accounts listed on the balance sheet (also known as the accounting equation).

Bank Reconciliation

A bank reconciliation compares your cash expenditures with your overall bank statements and helps keep your business records consistent. (This is the process of reconciling your book balance to your bank balance of cash.)

There are a few reasons the balance on your records may not be the same as the bank’s:

- When someone hasn’t yet cashed a check you’ve sent: The money owed from that check is still in your bank account – but it’s no longer yours to spend.

- Changes to bank accounts at the end of a month: This can happen when you withdraw or deposit money just before the bank sends a statement. Those changes to the account might not show until the following month’s statement.

- The bank deducts loan payments: The bank can deduct money for loans before you enter that information into your systems.

- Deposits in transit: Deposits you’ve made and recorded in your books that haven’t yet processed through the bank.

Bank reconciliation helps you identify these cases so you know exactly how much money is available to your business. It’s also needed to identify any cases of human error, bank charges and possible fraud.

Cash Accounting

Cash accounting is an accounting method where payment receipts are recorded during the period in which they are received, and expenses are recorded in the period in which they are actually paid. In other words, revenues and expenses are recorded when cash is received and paid, respectively.Cash accounting is also called cash-basis accounting; and may be contrasted with accrual accounting, which recognises income at the time the revenue is earned and records expenses when liabilities are incurred regardless of when cash is actually received or paid.

Cash Flow Statement

A cash flow statement analyses your business’s operating, financing, and investing activities to show how and where you’re receiving and spending money.

Capital

Capital refers to the money you have to invest or spend on growing your business. Commonly referred to as "working capital," capital refers to funds that can be accessed (like cash in the bank) and don’t include assets or liabilities.

Cost of Goods Sold

The cost of goods sold (COGS) or cost of sales (COS) is the cost of producing your product or delivering your service.COGS or COS is the first expense you’ll see on your profit and loss (P&L) statement and is a critical component when calculating your business’s gross margin. Reducing your COGS can help you increase profit without increasing sales.

Company Book Value

For a company, a simple book value is calculated by subtracting total liabilities from total assets. This may also be called net worth or book value of equity. More detailed book values take other factors into account, such as also deducting intangible assets.For example, Joe’s Plumbing Ltd has $2 million in assets and $500,000 in liabilities. The company’s book value is $2 million – $500,000 = $1.5 million.

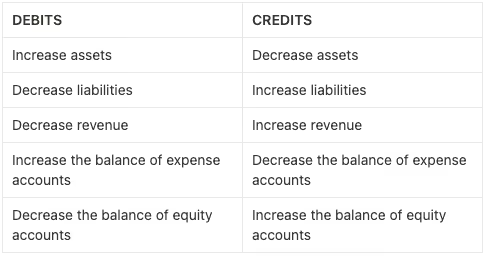

Debits & Credits

Not to be confused with your personal debit and credit cards, debits and credits are foundational accounting terms to know.A debit is a record of all money expected to come into an account. A credit is a record of all money expected to come out of an account. Essentially, debits and credits track where the money in your business is coming from, and where it’s going.Many businesses operate out of a cash account – or a business bank account that holds liquid assets for the business. When a company pays for an expense out of pocket, the cash account is credited, because money is moving from the account to cover the expense. This means the expense is debited because the funds credited from the cash account are covering the cost of that expense.Here’s a simple visual to help you understand the difference between debits and credits:

Depreciation

Depreciation refers to the decrease in your assets’ values over time. It’s important for tax purposes, as larger assets that impact your business’s ability to make money can be written off based on their depreciation.

Equity

Equity refers to the amount of money invested in a business by its owners. It’s also known as "owner’s equity" and can include things of non-monetary value such as time, energy, and other resources. (Ever heard of "sweat equity"?)Equity can also be defined as the difference between your business’s assets (what you own) and liabilities (what you owe).A business with healthy (positive) equity is attractive to potential investors, lenders, and buyers. Investors and analysts also look at your business’s EBITDA, which stands for earnings before interest, taxes, depreciation, and amortisation.

Expenses

Expenses include any purchases you make or money you spend in an effort to generate revenue. Expenses are also referred to as "the cost of doing business".

There are four main types of expenses, although some expenses fall into more than one category.

- Fixed expenses are consistent expenses, like rent or salaries. These expenses aren’t typically affected by company sales or market trends.

- Variable expenses fluctuate with company performance and production, like utilities and raw materials.

- Accrued expenses are single expenses that have been recorded or reported but not yet paid. (These would fall under accounts payable, as we discussed above.)

- Operating expenses are necessary for a company to do business and generate revenue, like rent, utilities, payroll, and utilities.

Fiscal Year

A fiscal year is the time period a company uses for accounting. The start and end dates of your fiscal year are determined by your company; some coincide with the calendar year, while others vary based on when accountants can prepare financial statements.

Financial Statements

Financial statements are written records that convey the business activities and the financial performance of a company. Financial statements include:

Balance Sheet

Profit and Loss

Trial Balance

Statement of Account

Account Detail

Aged Receivables

Aged Payables

Financial statements are often audited by government agencies, accountants, firms, etc. to ensure accuracy and for tax, financing, or investing purposes.

Gross Margin

Your gross margin (or

gross income), which is your total sales minus your COGS — this number indicates your business’s sustainability.

Journal

A journal is a place of record in which business transactions are recorded in chronological order. A firm may use several specialised journals, such as a purchase journal or sales journal to separately record transactions. A general journal can be used to record more general, lower-volume transactions.

Journals are the best source of information when researching the nature of business transactions, since they identify source documentsEntries made into a journal employ double-entry accounting, where balancing debit and credits are used. The entries also state the date, accounts impacted, and amounts, as well as an identifier for the source document.

Note : Eleven is using a single Journal per currency (at least one in base currency) and we are making use of Document Types to distinguish transactions (Customer Invoice, General, Vendor Invoice, etc..)

Journal Entry

A journal entry is used to record a business transaction in the accounting records of a business. A journal entry can be recorded in a journal. Posted Journal Entries will then be used to create financial statements for the business.The logic behind a journal entry is to record every business transaction in at least two places (known as double entry accounting). For example, when you generate a sale for cash, this increases both the revenue account and the cash account. Or, if you buy goods on account, this increases both the accounts payable account and the inventory account.

How to Write a Journal Entry

The structure of a journal entry is:

- A header that may include a journal entry number and entry date.

- Journal Entry Lines that will detail the account number and account name into which the entry is recorded.

The structural rules of a journal entry are that there must be a minimum of two line items in the journal entry, and that the total amount you enter in the base debit column equals the total amount entered in the base credit column.

Types of Journal Entries

There are several types of journal entries, including:

- Common Transactions. Common transactions, such as customer billings or supplier invoices, payments, receipts. These transactions are handled through specialised software modules that present a standard on-line form to be filled out. Once you have filled out the form, the software automatically creates the accounting record for you. Thus, journal entries are not to be used to record high-volume activities.

- Journal Entry Lines that will detail the account number and account name into which the entry is recorded.

- Compound entry. A compound journal entry is one that includes more than two lines of entries. It is frequently used to record complex transactions, or several transactions at once. For example, the journal entry to record a payroll usually contains many lines, since it involves the recordation of numerous tax liabilities and payroll deductions.

- Reversing entry. This is typically an adjusting entry that is reversed as of the beginning of the following period, usually because an expense was to be accrued in the preceding period, and is no longer needed. Thus, a wage accrual in the preceding period is reversed in the next period, to be replaced by an actual payroll expenditure.

- Cancel entry. This is typically an entry that is cancelled because there was an error on a posted entry.

Journal entries and attached documentation should be retained for a number of years, at least until there is no longer a need to have the financial statements of a business audited. The minimum duration period for journal entries should be included in the corporate archiving policy.

Liabilities

Liabilities are everything that your company owes in the long or short term. Your liabilities could include a credit card balance, payroll, taxes, or a loan.

Monetary / Non Monetary

A monetary item is an asset or liability carrying a value in dollars that will not change in the future. These items have a fixed numerical value in dollars, and a dollar is always worth a dollar. Monetary assets (such as cash and accounts receivable) and monetary liabilities (such as notes and accounts payable) have a fixed exchange value unaffected by inflation or deflation.A non-monetary item is an asset or liability that does not have a fixed exchange cash value but whose value depends on economic conditions.The differences between monetary and non- monetary items are given below;

Profit

In accounting terms, profit — or the "bottom line" — is the difference between your income, COGS, and expenses (including operating, interest, and depreciation expenses).

Profit and Loss Report

The profit and loss report / income statement presents the financial results of a business for a stated period of time. The statement quantifies the amount of revenue generated and expenses incurred by an organisation during a reporting period, as well as any resulting net profit or loss. The income statement is an essential part of the financial statements that an organisation releases. The other parts of the financial statements are the balance sheet and statement of cash flows.There is no required template in the accounting standards for how the income statement is to be presented. Instead, common usage dictates several possible formats, which typically include some or all of the following line items:

- Revenue

- Tax expense

- Profit or loss

- Other comprehensive income, subdivided into each component thereof

- Total comprehensive income

When presenting information in the income statement, the focus should be on providing information in a manner that maximises information relevance to the reader.

Revenue

Your revenue is the total amount of money you collect in exchange for your goods or services before any expenses are taken out.

Working Capital

Working capital measures a business’s ability to cover upcoming costs. The surplus or deficit is measured in dollars.Working capital is calculated by subtracting current liabilities (amounts owed within the next 3 to 12 months) from current assets. Current assets include cash the business has, plus payments due to come in, plus anything that could be sold quickly if required.

Year End Closing

At the end of a company's fiscal year, all temporary should be closed. Temporary accounts accumulate balances for a single fiscal year and are then emptied. Conversely, permanent accounts accumulate balances on an ongoing basis through many fiscal years.The most common types of temporary accounts are for revenue, expenses, gains, and losses - essentially any account that appears in the profit and loss. In addition, the Net Income for the Period account, which is an account used to summarise temporary account balances before shifting the net balance elsewhere, is also a temporary account. Permanent accounts are those that appear on the balance sheet, such as asset, liability, and equity accounts.At the end of the fiscal year, closing entries are used to shift the entire balance in every temporary account into retained earnings, which is a permanent account. The net amount of the balances shifted constitutes the gain or loss that the company earned during the period.Once the year-end processing has been completed, all of the temporary accounts have been emptied and therefore "closed" for the current fiscal year. A flag in the accounting software is then set to close down the old fiscal year, which means that no one can enter transactions during that time period. Another flag can be set to open the next fiscal year, at which point the same temporary accounts are opened, now with zero balances, and are used to begin accumulating transactional information for the next fiscal year.Thus, the only accounts closed at year end are temporary accounts. Permanent accounts remain open at all times.

Article Information

✍🏻 Written by: Eleven Support Team

🔎 Reviewed by: Noe Saglio

🗓️ Last Updated: November 12, 2025