%20(1).avif)

How to Compare Accounting Software for Your Accounting Firm

Learn the four key criteria that will help you cut through the jungle of accounting apps and choose the best one for your professional practice.

Managing cash flow across multiple currencies exposes businesses to exchange rate risk, forecasting gaps, and liquidity surprises. Here is how to get it under control.

Exchange rate volatility can quietly erode margins and undermine forecasts for any business operating across borders. This guide covers the key steps from auditing your currency exposure to hedging, banking structure, and forecasting, so you can manage multi-currency cash flow with a clear framework instead of reacting after the fact.

In this article

Managing global finances becomes much more complicated when you work with different currencies.

That’s why knowing how to manage cash flow in multiple currencies is so important for growing businesses.

Handling cash flow in different currencies is one of the toughest financial challenges a business can face.

Foreign Exchange volatility ranks among the top challenges for treasury organizations, with 46% of respondents citing limited visibility into global cash and financial risk exposures as their single biggest pain point.

If you do not have a clear plan, changes in currency values can slowly reduce your profits, make forecasts less accurate, and cause cash shortages that are hard to explain.

Multi-currency cash flow refers to the movement of money into and out of a business across multiple currencies.

This happens whenever a company invoices clients in a foreign currency, pays international suppliers, runs payroll in multiple countries, or holds cash reserves abroad.

The challenge is not just operational. Every time money moves between currencies, the business is exposed to exchange rate risk.

A payment expected in euros is worth a different amount in dollars depending on when it settles.

Multiply that across dozens of transactions, several currencies, and different settlement windows, and the cumulative impact on your actual cash position can diverge significantly from what your forecast shows.

For businesses operating across borders, multi-currency cash flow management is not a treasury edge case. It is a core part of financial operations.

→ Read about Cash Accounting: Definition and Current Scene

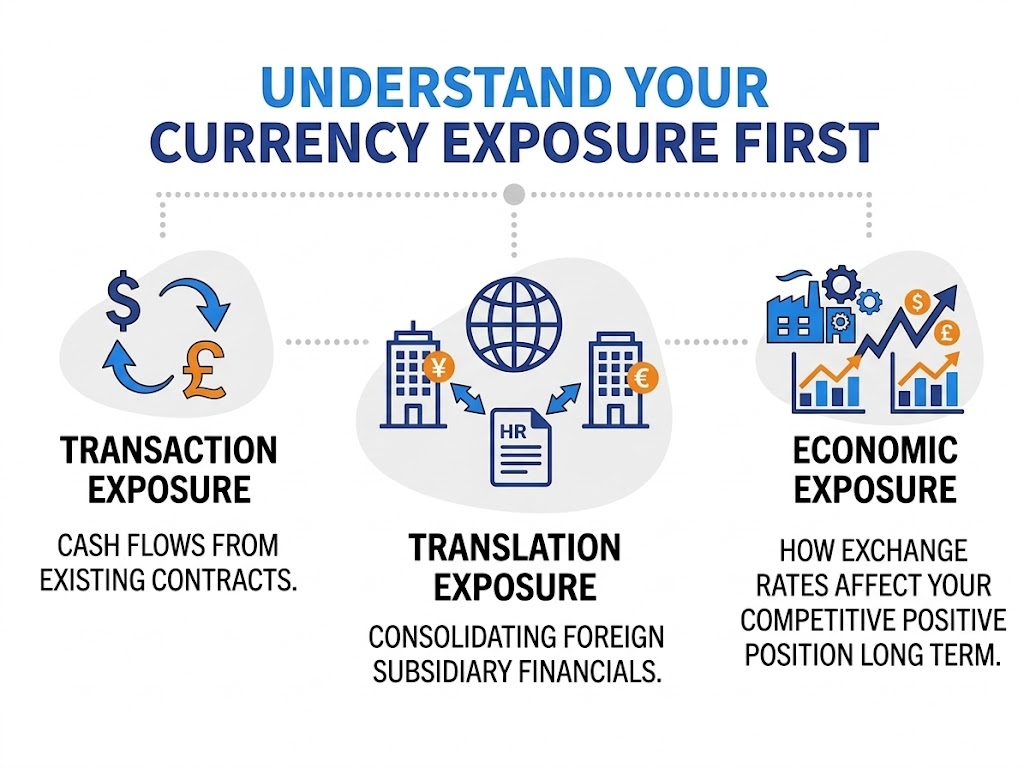

Before you can manage anything, you need a clear picture of where your exposure sits.

Basically, your currency exposure falls into three categories:

Most SMB’s and mid-market companies focus on transaction exposure and ignore the other two, which can lead to surprises at close.

Start by mapping every currency your business touches. That includes where you invoice, where you pay suppliers, where payroll runs, and where you hold reserves.

This map will be the foundation for everything else.

An exposure audit is the process of identifying and quantifying every currency-denominated cash flow in your business.

It gives you a factual baseline to work from, so that hedging decisions, account structures, and forecasting assumptions are grounded in what is actually happening rather than what you assume is happening.

Without it, you are managing Foreign Exchange risk blind.

To run an audit:

By completing this audit, you will see exactly where your main currency risks are.

When you know which currencies are most important, how much exposure you have, and where timing or market limits create risk, you can make better decisions about hedging, account setup, and cash flow planning.

This step helps you turn uncertainty into clear actions and builds a strong base for managing multiple currencies well.

→ Read about Why Small Businesses Need Multi-Currency Accounting Software

Managing cash flow across multiple currencies requires a structured approach. Here are seven key steps to help you stay on top of your currency exposures and optimize liquidity.

Holding local currency accounts in your key markets is the most direct way to reduce conversion costs and timing risk.

Rather than converting every payment to your home currency before sending it back out, a local account lets you receive in one currency and pay local expenses from the same pool.

This natural netting reduces the number of conversions you execute and limits the slippage that comes with each one.

The table below outlines different types of multi-currency accounts, their ideal use cases, and how long they typically take to set up, helping you choose the right structure for your business needs.

Choose the structure based on volume, not convenience.

A multi-currency fintech account works well for occasional transactions, but if a currency represents a significant share of your revenue, a local bank account with proper treasury controls is worth the setup time.

→ Read also: Why Small Businesses Need Multi-Currency Accounting Software

A single-currency forecast does not give you a reliable view of liquidity when a material portion of your flows is in other currencies.

Your forecast needs to show expected inflows and outflows per currency, by period, before conversion. This lets you see whether a shortfall in one currency can be covered by a surplus in another or whether you actually need to convert.

Currency-level views: Show each currency's net position by week or month. A consolidated view hides the detail you need to make decisions.

Conversion assumptions: Document the exchange rate assumptions used in each forecast. Using spot, forward, or budget rates will yield different numbers. Be consistent and explicit.

Conversion timing: When you plan to convert matters as much as how much you convert. Stagger conversions to avoid executing large trades when rates are unfavorable.

Stress scenarios: Model what your cash position looks like if your two or three most material currencies move 10–15% against you simultaneously. This is not unlikely in volatile markets.

→ Read also: How To Manage Cash Flow in Multiple Currencies

Natural hedging means structuring your business operations to reduce currency exposure before you ever call a bank about a forward contract.

It is cheaper, simpler, and does not require expertise in derivatives. Most businesses have more natural hedging opportunities than they realize. This table summarizes common natural hedging methods and how they help reduce currency exposure.

Start by identifying where your natural offsets already exist. Then look for process changes that could create more of them. Financial hedging should cover what remains, not substitute for operational discipline.

Once you have mapped your exposure and maximized natural hedges, the remaining risk is what you hedge with financial instruments.

The most common tools are forward contracts, options, and currency swaps. Each has a different risk and cost profile.

This table outlines common financial hedging instruments, what they do, and when to use them for managing residual currency risk.

A few practical rules: hedge exposures that are large enough to materially affect earnings, hedge at least 50–75% of your forecast exposure (not 100%, unless your cash flows are highly predictable), and document your hedge accounting policy before you start if IFRS or US GAAP treatment matters for your reporting.

Decentralized currency management, where each subsidiary or team handles its own Foreign Exchange, is one of the most common sources of inefficiency and unnecessary cost.

A centralized treasury function, or even a shared treasury policy, gives you netting benefits across the organization, better visibility into group-level exposure, and more negotiating leverage with banks.

Larger organizations set up an in-house bank or an intercompany netting center.

Subsidiaries invoice each other in a netting currency, net positions are calculated centrally, and only the net amounts are settled externally. This dramatically reduces the number of external Foreign Exchange transactions.

Smaller organizations achieve a similar effect by designating one team or person as the currency decision-maker, standardizing the tools and accounts used across entities, and setting a policy for when and how conversions are approved.

Even basic centralization, such as a single Foreign Exchange policy document shared across the business, reduces the execution variance that drives unnecessary costs.

Managing multi-currency cash flow manually in spreadsheets is possible at small scale. It breaks down fast. This table lists key functions, tool types, and example providers for managing multi-currency cash flow efficiently.

The most important integration is between your Foreign Exchange execution platform and your Enterprise Resource Planning.

If exchange rate data and transaction records do not flow automatically, reconciliation becomes a manual bottleneck and errors compound over time.

Currency management is not a set-and-forget function. Exchange rates move, forecasts shift, and hedges need to be rolled or unwound.

Weekly: Review open FX positions, upcoming settlements, and material rate movements against budget assumptions.

Monthly: Reconcile multi-currency accounts, update the forecast with actuals, and review hedge effectiveness.

Quarterly: Assess whether your hedge ratios and instruments still match your actual exposure profile. Adjust hedging policy if the business has changed materially.

Annually: Review banking relationships, platform costs, and whether your overall FX strategy is still fit for purpose.

Reporting should include realized and unrealized FX gains and losses separately from operating results.

Mixing them obscures business performance and makes it harder to evaluate the effectiveness of your currency strategy.

Eleven helps you manage multi-currency cash flow in a simple and transparent way.

With Eleven, you can see all your cash positions across every currency. This helps you spot risks early and take steps to protect your margins.

Your forecasts become more accurate, and your decisions rely on real-time data instead of guesses. This lets your finance team focus on strategy, not manual reconciliation.

When you centralize and automate currency management with Eleven, you reduce complexity and make operations smoother.

This lets your business respond quickly to changes in exchange rates, so you can manage liquidity better and feel more confident about your finances. Managing multi-currency cash flow becomes not just easier, but a real advantage.

Ready to take control of your multi-currency cash flow? Request a demo with Eleven today and see how simple it can be.

Multi-currency cash flow management is about understanding where your exposure sits, and building the operational and financial structures that reduce it.

The businesses that do this well tend to share a few things:

The steps in this guide are not sequential in the sense that you must complete one before starting the next.

Most businesses will work on several simultaneously.

What matters is having a coherent framework rather than reacting to exchange rate movements after the fact.

Related content

We are using cookies. Learn more.

%20(1).avif)